LESSON 4: Set Realistic Goals

From my online video tutorial:

SO YOU WANT TO DO CRAFTSHOWS…

16 CRUCIAL LESSONS I LEARNED

BY DOING CRAFT SHOWS

Instructor: Warren Feld

LESSON 4: SET REALISTIC GOALS

Making money at fairs and shows isn’t as easy as it seems. As Roland and Rolanda quickly found out. They thought all it took was to rent a table at any show or fair, lay out their jewelry, wait for customers to come by, and purchase their stuff.

All through the shows, they sat on chairs reading books, waiting for people to come by. They spent more money on inventory, packing, displays and travel than they ever made.

And they never developed any kind of plan of action.

Roland and Rolanda needed to set realistic goals:

– (1) how much money did they have to get started and sustain themselves?

– (2) what was their break-even point?

– (3) what did they need to prepare themselves to “sell”?

- (4) what amount of repeat business and follow-up sales were they looking for?

BUDGET

How much money will you need?

Make a list of all possible costs. There are the obvious like transportation, lodging and meals, and the costs of displays, packing and marketing, and the costs of the parts used to make the pieces which sell.

Entry fees will vary widely from show to show. They cold cost $25/day up to $400 and up per day. They could go as high as $5000 per day.

If you have a specific craft show in mind, review their rules, and what they entry fees cover, and do not cover.

What are the costs of extras, like electricity, tables, special lighting? Do they also collect a percent of sales? Do they offer special services, like booth sitting, for extra fees? Is parking free, or do they charge? Do you need to provide additional insurance? Will you need to purchase special licenses, registration and permits, such as an out-of-state wholesale license?

THERE ARE TWO TYPES OF COSTS TO ACCOUNT FOR:

Fixed Costs and Variable Costs

You need to prepare a budget to be sure you can pay for what you are committing yourself to.

You will need display supplies, packing supplies, marketing and promotion supplies, and probably some food and drink for yourself. You will be traveling. You may have to stay overnight somewhere. You will probably have some credit card finance charges and cell-phone charges associated with sales you make. You may need to pay someone to help you staff your booth. You probably will be paying various fees — entry, electricity, table rental. And you will need enough money to buy enough supplies to make up your inventory.

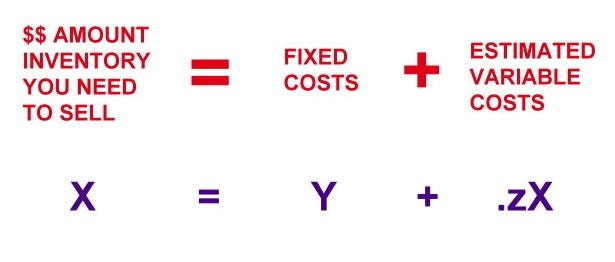

Your breakeven point is when your revenues = your costs.

How much money do you want to make?

At the very least, you want to come home from the show and breakeven. That is, you want to cover all your costs.

So, in your budget, you have begun to list all your costs.

Now, how much inventory will you need to make, and sell, in order to breakeven?

Inventory: Bring 4x what you need to sell

At this point, we are going to talk about inventory in terms of retail prices, not in terms of numbers of items, and not in terms of wholesale costs.

Our total inventory would equal the total of all retail prices (=the prices you are selling each piece at), if every piece sold.

A good rule of thumb for figuring out how much inventory to bring is this:

You will need to bring with you, at a minimum, 4 times the inventory (=total retail dollars) you hope to sell.

YOU WILL NEED TO BRING WITH YOU, AT A MINIMUM, 4 TIMES THE INVENTORY YOU HOPE TO SELL.

For example, if you need to sell $200.00 of merchandise to breakeven, you will need to bring $800.00 of merchandise with you. Again, $800.00 is the total of all the retail prices of what you bring.

If you want to take in another $100.00 of sales on top of your breakeven, then you will need to sell $300.00 (=$200 + $100) of merchandise, and then you will need to bring a total of $1200.00 (=$800+$400) of inventory. This is $400.00 more inventory that you would need to bring to make one hundred more dollars over your breakeven point. Again, $1200.00 is the total of all the retail prices.

BREAKEVEN ANALYSIS

I want to introduce you to a quick and dirty breakeven analysis. I call this “Quick and Dirty” because we are using imperfect information. However, this imperfect information is good enough to help us make a decision whether a particular craft show is worth the risk.

Your breakeven point is where you have sold enough inventory to cover your costs. That is, the total retail dollars you have taken in equals the sum of your fixed plus your variable costs.

We use our quick and dirty breakeven analysis to answer the question: How much inventory do I need to sell in order to breakeven?

Let’s familiarize ourselves more with the components of the formula, and then review the math.

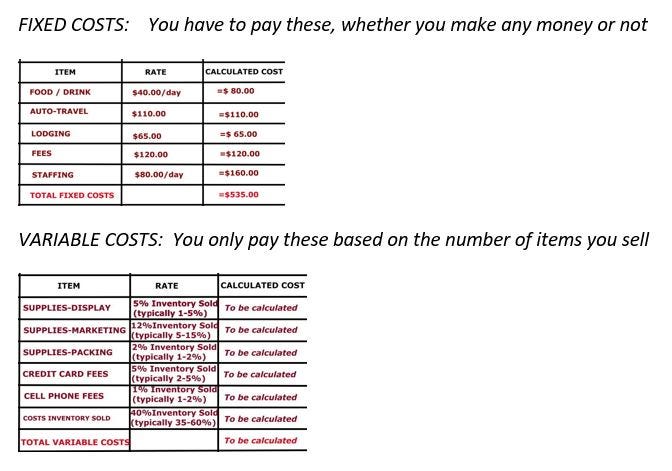

FIXED COSTS

Fixed costs are costs that remain the same, regardless of how many items you sell at your craft fair.

Fixed costs include things like fees, travel, food, and staffing. Again, you have to lay out this money for fixed costs whether you made no money at all, or made a bucket full of money at your craft fair.

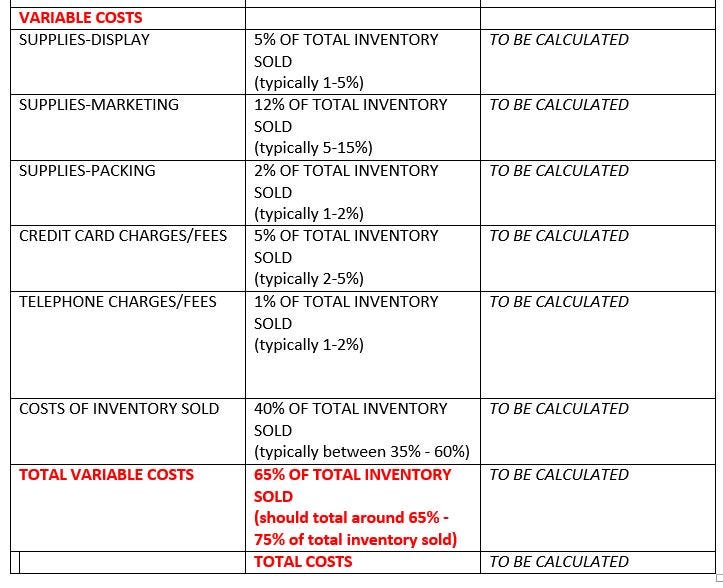

VARIABLE COSTS

Variable costs are costs that get incurred when each unit is sold.

Thus, variable costs fluctuate based on the number of units sold. If you seel very few pieces, your variable costs are small. If you sell a lot of pieces, your variable costs will be much higher.

Variable costs include special packaging and displays, brochures and business cards handed out with each sale, credit card fees you are charged by the banks after each sale, and the cost of the parts used to make each piece that has sold.

We estimate variable costs using some industry standards about the percent of total retail price these costs are associated with.

NOTES:

When we calculate the cost of inventory, we differentiate between the cost of those pieces which we actually have sold from the cost of those pieces we did not sell.

For purposes of developing a budget and calculating a breakeven analysis, to help us decide whether a particular craft show is worth the risk, we focus only on the estimates based on what we sell.

From an overall business standpoint, because you will want to bring 4x the inventory of what you predict will be sold, and these additional out of pocket expenses associated with the pieces which would not be sold have not been included in our breakeven analysis, you will need to be realistic, whether you can afford the show, or not.

INVESTMENT COSTS

There are some additional costs you will incur which are also not included in our breakeven analysis. I’m going to call these “investment costs.” Investment costs are things you pay for which have to last a very long time, and which you will use at many, many craft shows.

These include “long term assets”, such as buying tables na dchairs, a tent, and display cases.

These also include “long term liabilities”, such as paying down loans and credit card charges over a longer period of time.

We do not include these investment costs in our breakeven analyses.

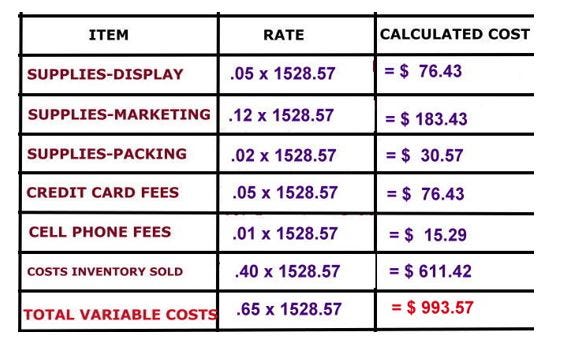

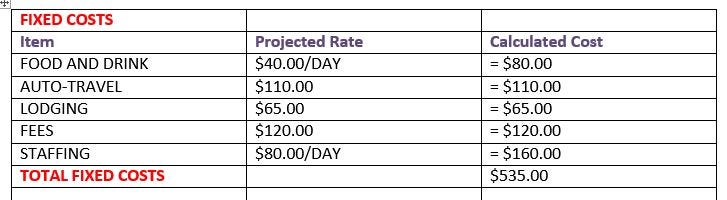

FIXED AND VARIABLE COSTS LAID OUT WITHIN A BUDGET TABLE

Say you will be doing a 2-day craft show out of town, 200 miles away from home. And you will need to hire 1 person to help you. Let’s look at our budget for doing this particular craft show.

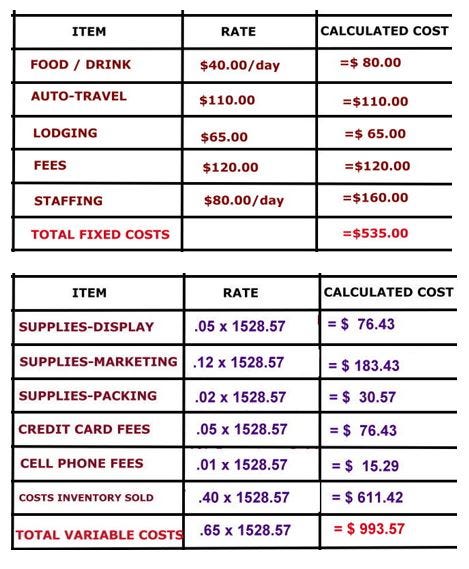

You have budgeted for your fixed and variable costs as shown in the table above. I have plugged in some typical numbers into this budget table.

Our fixed costs are relatively easy to figure out.

Our variable costs, however, will have to be estimated. These variable costs are keyed off the retail prices you set for your jewelry. We will use some industry percent of price standards, as well as our breakeven analysis formula, to help us figure out the “TO BE CALCULATED” variable costs in our budget table.

For example,

I have used 12% as the proportion of the total retail price that would be spent on marketing costs. These costs would include brochures, business cards, a post card mailing, some promotional ads, some effort to contact previous customers to let them know you will be at this craft show. The industry standard for marketing ranges between 5 and 15 per cent.

If you are getting started, you can use my numbers presented in this table. After you have done a few craft shows, you can begin to analyze your own sales and cost data, to develop what are called multipliers for each variable line-item category.

Again, our quick and dirty analysis is keyed off our retail prices.

I am assuming that you already know how to set fair and reasonable prices for your merchandise. If not, I would suggest reviewing my PRICING AND SELLING video tutorial.

BREAKEVEN ANALYSIS

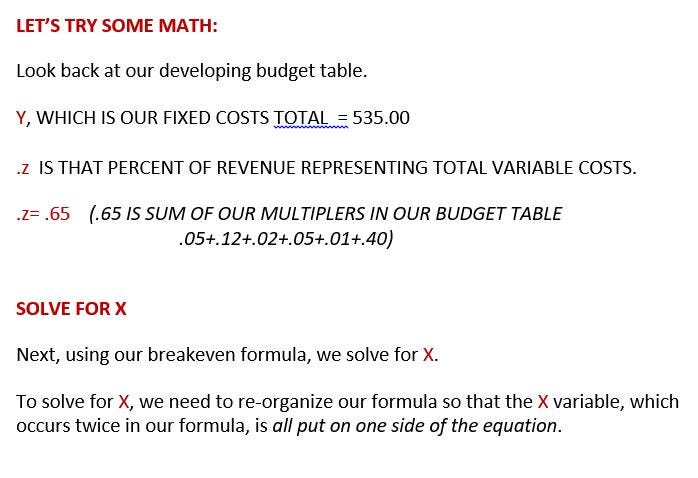

LET’S TRY SOME MATH:

THIS IS HOW WE SOLVE THIS FORMULA:

Let’s review this breakeven formula application again, in English.

For those of you who haven’t had algebra, or are somewhat math-phobic, I want to go over the mathematical analysis in more English terms. It is important to understand the concepts, and to understand how to do the math.

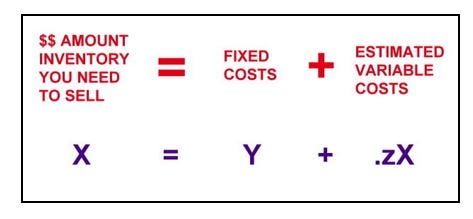

First, we have the breakeven formula itself. Basically, it says:

100% of Breakeven revenue

Equals

The Total of all our costs.

Some of these costs are fixed, meaning we have to pay for them, whether we make any money or not.

Some of these costs are variable, meaning we only incur these costs when we sell something. The amount of variable costs “Varies” based on how much we sell.

We are trying to figure out how much we need to sell in order to breakeven. We can easily figure out our fixed costs. We estimate our variable costs as a percent of revenues.

In this particular example,

Our fixed costs were $535.00. So, Y = $535.00

We estimated our variable costs as 65% of revenues. So our variable costs = .65 times X.

This is all the information we need to do the algebra in the formula and figure out our breakeven revenue=costs point, which we have called “X”.

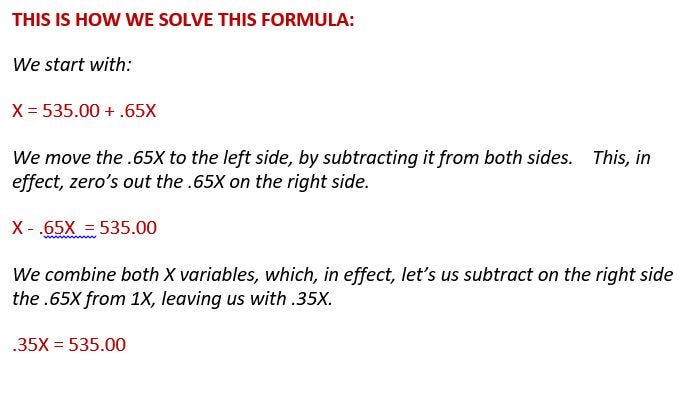

We begin to re-state the formula as:

100% of revenue equals $535.00 + 65% of revenue.

So, we continue to play with the formula so that we get:

Total Breakeven Revenues on one side of the equals sign, and everything else on the other side.

We have to do this is a few steps.

We re-write the formula again:

100% of revenue minus 65% of revenues equals $535.00.

And we simplify this a little by writing the formula as:

100% minus 65% times revenues = $535.00

And simplifying the formula even more, we subtract 65% from 100% and get 35%, and the formula reads:

35% times revenues = $535.00

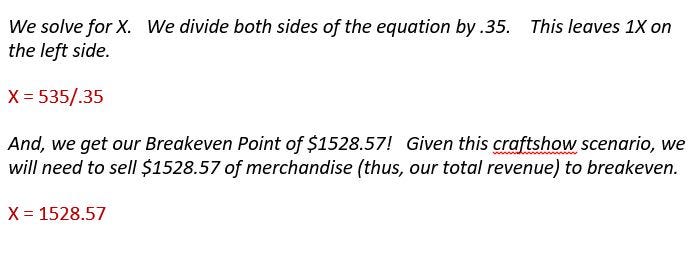

Since we want to end up with 100% of revenues on one side of the equation, and the dollar amount that this 100% equals on the other side, we have to do one more math step.

To change .35X to 1X, we have to divide it by .35.

Mathematically, if we do something to one side of the equation, we have to do it to the other side, as well.

That’s how we get:

100% of revenues = $535.00 divided by 35%.

And the answer is that our breakeven revenue, where our sales equals our costs, is

$1528.57

So, to breakeven, we would need to sell a retail total of 41528.57 of merchansie at our 2-day show. To sell that much inventory, we would need to bring about 4x that much, or $6,000.00 of inventory with us.

While we do not include the costs of this additional inventory, and which we assumed would not sell, we still need to anticipate in our realistic goal setting process, the financial impact of all this.

Let’s update our budget table for this 2-day craft show example:

ONE MORE EXAMPLE

Now, let’s review our breakeven analysis with another example.

Say you are doing a 1-day craft show, close to home, low fees, you bring your own tables, and you don’t need electricity, and don’t need extra staffing. Also, you don’t plan on doing a lot of marketing.

First, you begin to set up a Budget.

Here we have fixed costs equal to $70.00.

Our variable costs we estimate to be 54% of our total revenues.

Next, we calculate our breakeven point, using our quick and dirty formula.

We see our breakeven point is $152.17. And using our rule of thumb about how much inventory to bring, we need to bring 4 x $152.17, or about $600.00 of inventory.

The Next Question To Ask Ourselves: How Much Profit Do You Want To Make?

How much more money do you want to make above and beyond your breakeven point?

You don’t just want to breakeven. You want to make a profit. At our breakeven point, we have covered both our fixed costs and our variable costs. Our fixed costs are now all paid for.

As we bring in more addition revenues, we will have more variable costs to cover, and only based on how much more we sell.

Example 1 above: In our first example, our breakeven point was $1528.57.

In this example, 65 cents of each dollar in price that was earned was spent on variable costs, and 35 cents on each dollar earned was spent on fixed costs.

As we go beyond our breakeven point, and become profitable, again in this example, we would be spending only 65 cents out of each additional revenue dollar for variable costs.

We would have no more fixed costs.

If we had sold one more dollar, we would have had 35 cents remaining. We could have used that remaining 35 cents out of each dollar of additional revenue to pay for some of our investment costs, as well as pay ourselves something.

Profit Goal

How much of a profit goal you want to set is your personal choice. However, I like to tell students that breaking even at the show itself is OK, if you also have strategies in place to generate follow-up sales, either through repeat sales between shows, or repeat sales at the next show.

WHAT DID THEY NEED TO PREPARE THEMSELVES TO “SELL”?

Selecting and doing craft shows requires research and planning. And it requires an ability to keep up a good “Retail Personality” while standing on your feet for ong hours, sometimes when it’s too hot or too cold or too windy and dusty.

Selling Jewelry requires a different mind-set than Creating Jewelry. If you don’t have the personality for Selling, bring a friend with you who does.

WHAT AMOUNT OF REPEAT BUSINESS AND FOLLOW-UP SALES SHOULD YOU LOOK FOR?

A good goal to set is to generate repeat business equal to 25%. So, if you have 10 sales at the show, your goal would be to get 3 repeat sales. These could occur when the customer contacts you between shows. These could also occur at the next show you do, when the customer buys from you again.

You will make a might higher profit and experience better long-term outcomes, through repeat business. With repeat business, you can considerably lower your variable costs, particularly those associated with marketing. Because of this, that 2nd or follow-up sale is often more important than that 1st sale at the show.

Lesson 4 was to set Realistic Goals.

It is OK to start small. To start locally. To gradually take on bigger and bigger shows, while you are establishing your reputation and building a following.

You obviously want to keep your expenses to a minimum, and there can be some steep up-front costs, such as creating a sufficient inventory.

Starting small gives you a chance to test out your ideas about costs, whether you like doing craft shows, whether there is a good fit between your merchandise and the shows, and whether there is a good fit between your personality and doing craft shows.

When you start, you might be able to share booth space with another friend who has a business, and share some of those other fixed costs, like travel and fees.

Do your homework when selecting craft shows which fit well with your goals and your budget. Figure out your breakeven point, and how much inventory you need to bring to make a profit.

As Roland and Rolanda should have done.

Other Articles of Interest by Warren Feld:

Should I Set Up My Craft Business On A Marketplace Online?

The Importance of Self-Promotion: Don’t Be Shy

Are You Prepared For When The Reporter Comes A-Calling?

A Fool-Proof Formula For Pricing And Selling Your Jewelry

Designer Connect Profile: Tony Perrin, Jewelry Designer

My Aunt Gert: Illustrating Some Lessons In Business Smarts

Copyrighting Your Pieces: Let’s Not Confuse The Moral With The Legal Issues

Naming Your Business / Naming Your Jewelry

Jewelry Making Materials: Knowing What To Do

To What Extent Should Business Concerns Influence Artistic and Jewelry Design Choices

How Creatives Can Successfully Survive In Business

Getting Started In Business: What You Do First To Make It Official

I hope you found this article useful. Be sure to click the CLAP HANDS icon at the bottom of this article.

Also, check out my website (www.warrenfeldjewelry.com).

Subscribe to my Learn To Bead blog (https://blog.landofodds.com).

Visit Land of Odds online (https://www.landofodds.com)for all your jewelry making supplies.

Enroll in my jewelry design and business of craft video tutorials online. Begin with my ORIENTATION TO BEADS & JEWELRY FINDINGS COURSE.

Check out these two other tutorials:

Pricing and Selling Your Jewelry. Learn an easy-to-use pricing formula and some marketing tips.

So You Want To Do Craft Shows… 16 Lessons I Learned Doing Craft Shows. Understand everything involved and make the smart choices.

Add your name to my email list.