Abstract:

Financial management includes all the things you need to do in order to determine your Return On Investment (ROI). It mostly involves a system of data collection, monitoring and analysis methods employed by any successful business. This system relates risks to rewards. Activities in this kind of system include things such as general accounting and bookkeeping, inventory management, and record keeping. These include things you do to establish and maintain formal relationships with employees, independent contractors and suppliers. These include things you do to secure your money, such as with banks, financial institutions, and even such things as crowd-funding online. This is a lot of numbers and activities, and often, when we look at why people fail in business, it is often because of a generalized fear of getting in control of all this. Successful business people and successful businesses need to foster a culture which promotes a growth mindset. Simply this is a culture where you have permission and encouragement and confidence to take risks.

A Focus On Your Return On Investment (ROI)

You put a lot of time, effort and resources into designing pieces of jewelry and building up your business. This all has a cost to you in time, money, and even relationships. You want a Return On Investment (ROI). You want to see some benefits that exceed your costs. Joy, happiness, contentment, money, security, less stress, more opportunities and more challenging opportunities to be creative, more fulfilling relationships.

When you take your creative endeavors and turn them into a business, the core focus primarily rests on increasing your returns on investments (ROI’s) through smartly and strategically managing your finances. You want to set into place various management structures and routine data collection procedures to assist you in managing risk and maximizing rewards. You want to minimize the effects of uncertainty on your business.

Sometimes, creative people think that some people are born to take risks, manage them and live with them, and others are not. This is not true. Having a business sense is not something innate or genetic. It’s something that is learned over time, often with a lot of trial and error, many failures, but key successes, as well. There is no reason, if this is something you want to do, to shy away from thinking about or attempting to monetize your jewelry as a business.

Towards this end, you want to get a good handle on such things as:

- Understanding risk and reward

- Tracking your costs and revenues

- Tracking your inventory

- Other record keeping

- Employees and Independent Contractors

- Banking, Insurance and Credit Card Processing

- Getting Terms

- Getting Paid

- Crowd-funding

- Fostering a Growth Mind-set

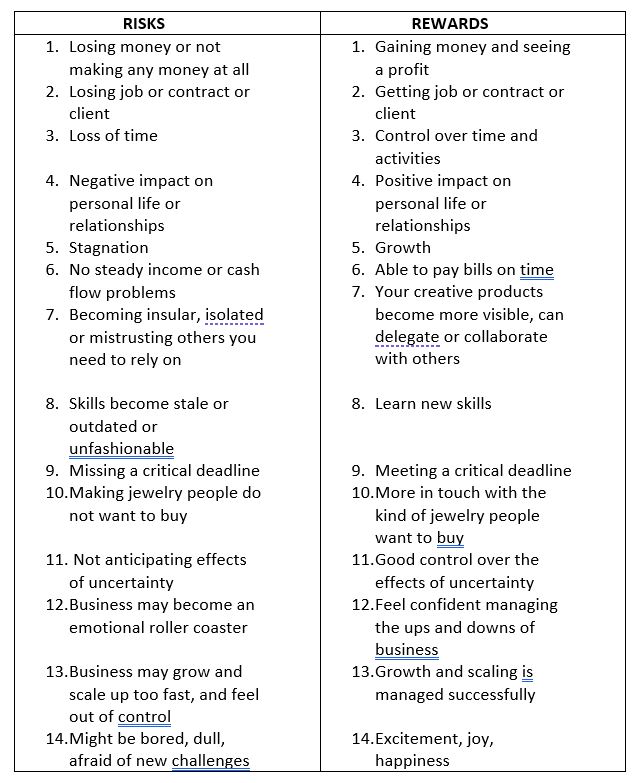

a) ROI: Understanding Risk and Reward

It is important to understand risk and reward, and how to manage these. Part of managing these is putting into place systems which collect necessary data – primarily about costs and revenues – and evaluating the data and its desired impact on everything you are trying to achieve in your business. Anyone can do this. But jewelry designers who foster a growth mind-set are often better at managing risk and reward.

What Is Risk and What Is Reward

Risks and rewards are gambles. They are probabilities. Chances. They help define the likelihood for determining whether what happens next will hurt you or help you.

Risk is the likelihood that you will lose either or both tangible rewards (money) and intangible rewards (success, happiness).

Rewards are the profits, again tangible (money) or intangible (success, happiness), you receive from taking risks.

Usually, the greater the risks you take, the greater the rewards earned. But this is not a guarantee. Losses can occur, usually resulting from the failures to properly manage the relationship between risks and rewards.

Risk management is important in every business because without it, that business cannot clarify what goals it needs to set, and what steps it needs to take towards meeting those goals. There are more things to do on a day-to-day basis than you could possibly do and get done. Risk management helps you narrow down the tasks to those most likely to have the greatest rewards.

Risks and Rewards must be managed in a deliberate, rational, and day-by-day way. Routinely. With fore-thought and organization. This means collecting data. This means analyzing data. This means closely looking at risk and evaluating whether it makes sense, or not, to continue doing what you are doing, or what you want to be doing. Is it sufficiently rewarding or profitable? What is the opportunity cost? That is, you could be expending the same amount of resources (time, motivation, money) doing something else that might have a greater return.

Any business is fraught with risk. If it were easy to start a business, everyone would do it. But it is not. Again, it requires routinely collecting and evaluating data. It takes you out of that creative mode and way of thinking, and plops you down into a very different administrative one. In order to sell a piece of jewelry, you have to begin to deal with things like marketing and promotion, production, distribution, inventory management, investments in tools, parts, displays and equipment. You need to closely track all your costs and all your revenues. It means taking chances you might lose money or fail. This is scary.

When managing risks, it is important to remember:

- Don’t confuse Risk with Fear. Fear keeps you from doing things. Risk aids you in asserting some control over uncertainty.

- Simply be aware that both Risks and Rewards exist. Where there are greater rewards, there are usually also greater risks.

- Yes, risks are risky, but should not be reckless.

- Make decisions based on the relationship of risks to rewards. It is not the number of pieces of jewelry you make. Rather it is the average return you get from each piece of jewelry you make, given the costs and investments you made in order to finish that piece of jewelry and sell it. This type of information will clue you into such things as what might happen if you too aggressively seek rewards, or too timidly accept risks.

- Don’t put all your eggs in one basket. Diversify the types of jewelry you make, designs you do, parts you use, markets you seek to exploit.

- Keep things simple. There is a lot of data, systems and subsystems of information to manage. Things which help keep things simple:

- standardization of forms, collection procedures, the ways data are organized

- use of summary indicators like totals, averages, means, mediums, rates, trends

- routines developed for procedures and administration

How Do You Measure Risk and Reward

As a jewelry designer, you will be measuring risks and rewards in a few different ways.

- Measuring Risk and Reward: General accounting

- Measuring Risk and Reward: Financial Management

- Measuring Risk and Reward: Inventory Management

- Measuring Risk and Reward: Pricing

- Measuring Risk and Reward: Impression Management

1) Measuring Risk and Reward: General Accounting

You will set up a General Ledger (G/L) to track your revenues and expenses, and liabilities and assets. This is like setting up a giant table or spreadsheet. You enter every piece of information into this table or spreadsheet that represents some kind of expenditure to you or some kind of revenue received. Below I go into more detail about setting up a General Ledger.

2) Measuring Risk and Reward: Financial Management

Here you try to reduce things you do to a series of rates and trend-lines. It is NOT the number or dollar amounts of your sales. Instead, it is your rate of sales. Your rates of inventory reduction and replenishment. Your accumulated debt to earnings. Breakeven analysis. Trends in gross profit and net profit.

For some rates, management means maintaining a constant velocity or turn in the rate. For example, if you need to sell a minimum of 6 pieces of jewelry each week to breakeven, are you able to maintain at least this rate every week in the year? If not, for those times in the year where the velocity of this rate might slow down, what else can you do instead to maintain your business at least at the breakeven point?

For other rates, management means maintaining an upward trend or trajectory, even though some weeks the data may decline. Especially when you first get started in business, your gross profit and net profit might be low or even negative numbers. The trend line is more important than the specific monthly numbers.

Leverage. A related concept in financial management is leverage. This is the degree you leverage someone else’s money to make money for yourself. You might be paying for some of your inventory, equipment, furnishings or other business expenses using a credit card or relying on a bank loan or leasing where you do not have to front all the costs all at once. You might be listing your jewelry on someone else’s website or marketplace where they are paying internet and website maintenance costs. You might be co-marketing your jewelry with someone else who sells a product which can be integrated with yours where you thus are sharing the costs. You might be buying inventory on terms, say NET 30, where you do not have to pay for the inventory for 30 days. You might maintain bare minimums of inventory items, where you depend on your suppliers to provide just-in-time shipments, thus having your suppliers foot the bill for a lot of storage costs.

In each case, someone else has made investments in things that either you do not have to, or you do not have to all at once. Sometimes, you pay for some of these over time. Othertimes, the synergistic effects create payments for all parties above and beyond what each could do on their own. All of this is called leverage.

We have to monitor leverage, as well, to be sure the rewards we get do not exceed the risk we undertake to get those rewards.

3) Measuring Risk and Reward: Inventory Management

There are three important things to understand about inventory up front:

- Inventory is a placeholder for money. You paid for your inventory, and you get that money back when you sell it.

- As a jewelry maker and designer, you will have a bi-furcated inventory, a) an inventory of finished pieces ready for sale, and b) an inventory of parts and pieces of jewelry not ready for sale.

- An inventory of digitized files and applications.

Holding inventory ties up a lot of money. This money is in the form of parts, perhaps restricting and constricting you in what colors, styles, materials, components and the like you will be able to use when designing a piece of jewelry. Too much or too little of inventory – or the right inventory for the moment – can break your business.

This all means that inventory is something that needs to be monitored and managed. Your goal is to minimize the cost of holding inventory. This involves figuring out ways to know when it is time to replenish inventory, change out and update inventory, or buy more materials to manufacture inventory. After all, you want to prevent these kinds of things from happening…

- Lose sales

- Hurt cash flow

- Buy too many things which don’t and won’t sell

- Create storage problems, including prevention of deterioration, such as plated finishes which fade over time

- Needing cash, but it’s all tied up in inventory – you can’t eat beads

- Reduce your profitability

- Reduce your resiliency – that is, an ability to adapt to fashion, style, demand and culture changes

- Losing that balance between efforts directed at inventory management with efforts required for general administration, marketing and promotion

4) Measuring Risk and Reward: Pricing

The price you set for each piece of jewelry has to be based on all the costs you incur. Not just the costs of the parts. Not just the time you put in. All the costs. These include, parts, labor and what is called overhead. Overhead is everything else: electricity, heat, rent, business travel, wear and tear on tools and equipment, and the like. It is not cost-effective to have to track each and every one of these overhead costs separately, so we typically estimate them using a formula. From a management standpoint, this formula needs to make sense and come close to its approximation. It has to be defensible.

5) Measuring Risk and Reward: Impression Management

Much of what we do these days is digital. We promote and sell our pieces on line. This might be directly through a website. It might be through social media. It might be through an auction site.

In the digital world we track and manage impressions (often referred to as eyeballs). Measures of risk in the digital world include concepts like Costs Per Click (CPC), Costs Per Impression (typically 1,000 impressions)(CPI), Adds To Cart (ATC), Cost Per Add To Cart (CATC), conversion rate (relates number of visitors to visitors who actually buy something), costs to maintain current conversion rate, and so forth.

Given the velocity or trends in these rates, and the returns on investments for you (such as costs of maintaining a website, marketing and promotion, supporting an inventory, handling money and credit cards, costs of shipping), you ask yourself questions about your various business and marketing strategies, your user experiences, and user impressions. What is it costing you to persuade people to take a look and to buy?

Some of these analytics will be provided to you in stats packages you can integrate with your site. Others will involve collecting data yourself, and analyzing them, usually in spreadsheets you create.

Next, you need to translate your understanding of risks and rewards into systems of data collection and analysis, beginning with the basics of tracking the flow of money in terms of costs and revenues.

b) ROI: Tracking Your Costs and Revenues

You set up an accounting General Ledger to track revenues and expenses, and assets and liabilities. Your goal here is to adequately account for your expenses and revenues, and your liabilities and assets.

What are business revenues?

Business revenues include all the money coming into your business, including payments for products and services, interest on bank accounts and investments, rent you charge others to use your space or equipment, royalties you get from intellectual property.

What are business expenses?

Business expenses are ANYTHING THAT HAVE TO DO WITH OR RELATE TO OR CONTRIBUTE TO MAKING A PROFIT.

You might want to secure copies of IRS publications that define each business expense and how it should be accounted for.

What are business assets?

Business assets are the current values of your physical property, from desks to chairs to computers to printers to major software packages. These are things which depreciate, that is, lose value over time.

A key asset is your inventory. If you are selling finished jewelry, your inventory will include all your works-in-progress as well as your finished pieces. For some jewelry businesses, it might become a little confusing to differentiate between your supply of parts and your jewelry, especially if you only assemble pieces after orders are made. On a yearly basis, the IRS only lets you deduct the costs associated with finished jewelry pieces sold. The rest of the inventory is treated like it is cash. You will need to decide what exactly you call inventory and what other supplies you call supplies. (See COST OF SALES section below).

What are business liabilities?

These are things the business owes money on, from short term net-30-day payments to suppliers to long term credit card bills and bank loans and leases.

BUSINESS USE OF A HOME: Many jewelry designers work out of their homes. While these expenses are red-flagged by the IRS, tax courts have consistently ruled that Congress intended to be very liberal and kind to these expenses.

You would compute the proportion of “business use” space in your home relative to your home’s total space. This space could be a whole room or part of a room. This space must only be devoted to business, not personal use. Based on this proportion, you allocate your mortgage or rent, your heating, A/C, water, sewer, and other maintenance costs to your business expenses.

Example: Your home is 1000 sq ft. The room you use for your business is 100 sq ft. So your business “use” expenses would be 10% of your rent/mortgage, 10% of your utilities, 10% of you lawn maintenance, 10% of repairs, etc.

For some expenses, you cannot use the straightforward proportion percentage. If you use a computer, it is a better idea to have a separate one that you use for business, than for personal. If you use one for both, you have to maintain a use log, and, based on “time the machine is used for business vs. personal”, you allocate the costs and depreciation of the machine to your business. Telephone costs are allocated based on the proportion of business calls to all calls each month.

Don’t be shy about what to call a legitimate business expense at your home. Picture a real store. If they have to mow the lawn, you would have to mow the lawn at your home. If 10% of your home were devoted to business, then 10% of your lawn mowing expenses would also qualify. Home repairs, fixing the roof, mortgage, insurance and the like would be legitimate. At the same time, if you have little income, do not declare these expenses with the sole purpose of gaming your tax liability.

SETTING UP A GENERAL LEDGER (G/L):

When you are just starting, you can set up a spreadsheet to track your expenses and revenues or even use a ledger book bought at a local office supplies store. Or you can purchase some inexpensive software apps. Many accounting apps have been moving to a “rent” rather than “purchase” model, where you pay a monthly fee to use their apps.

With a General Ledger, you are basically creating a giant table for the year. The rows are the days of the month. The columns are your revenue and expense categories. You also build in some summary formulas, such as the total Revenue for each month.

There are single-entry accounting systems and double-entry accounting systems. If you are just getting started and using a ledger book or spreadsheet, using a single-entry system where you record revenues and expenses only is fine. If you are using an accounting application, these typically are set up as a double-entry accounting system. Here, part of the ledger accounts for revenues and expenses and the other part of the accounting system will duplicate this information in the form of assets and liabilities. When you are making $6,000 – 10,000 per year in sales, you will want to graduate to the double-entry system. It is a straightforward step to evolve a single-entry to a double-entry system.

IN A SINGLE-ENTRY ACCOUNTING SYSTEM, you set up a spreadsheet, and track each of all your revenues and all your business expenses. The rows are days of the month and the columns are your various revenue and expense accounts. Each different revenue and cost is referred to as an account (or line item). All together, these accounts get assigned unique ID codes, and get organized into a Chart of Accounts. Each revenue or expense entry gets tagged with a specific ID code, and entered into a General Ledger (of Accounts).

Picture your G/L as a very large table. Again, the columns of the spreadsheet are these revenue and expense accounts. The rows are the days of the month. You should compute subtotals for each column at least once a month. If your business is a busy one, you should compute subtotals for each column weekly. You should also keep a running subtotal of year-to-date information.

| Revenue-Sales | Revenue- Classes | Consumable Supplies | Telephone | Rent | |

| 1/1/18 | 0.00 | 12.00 | |||

| 1/2/18 | 63.00 | 35.00 | 6.00 | ||

| 1/3/18 | 42.00 | ||||

| 1/4/18 | 190.00 | 29.00 | |||

| 1/31/18 | 43.00 | 150.00 | 750.00 | ||

| Jan Totals | 338.00 | 35.00 | 47.00 | 150.00 | 750.00 |

| Jan Avg | 67.60 (/5) | 7.00 (/5) | 9.40 (/5) | 4.84 (/31) | 24.19 (/31) |

What Accounts and How Many Accounts Do I Need?

You set up a sufficient number of accounts in order to satisfy two sometimes competing needs. You should be able to glance over your general ledger each month and come away with some good understandings of how your revenues and costs relate to your business strategies and programs. This is called good financial management. If you have too many accounts, financially managing them becomes more and more difficult.

You also want to anticipate issues of IRS auditing. You want clear categories, and maybe more categories than is easily managed from a financial standpoint. The IRS will suggest specific categories. You are not required to use them. You can use some of them, all of them or none of them. For example, I use one category I call OCCUPANCY, where the IRS has separate categories for INSURANCE, UTILITIES, MAINTENANCE.

| Examples of Accounts a) Revenue (sales, rents, royalties, teaching) b) Cost of Sales (special packaging, shipping inventory to you, commissions) c) Employee (wages, benefits, federal taxes, state taxes) d) Other Expenses (supplies, travel, marketing, fees, shipping things to others) f) Assets (Cash, Inventory, Bank Accounts, fixed like computer or table) g) Liabilities (Credit card debt, bank loan; money you owe your suppliers) |

REVENUE ACCOUNTS

The IRS has one revenue account. From a financial management standpoint, I like to have several revenue accounts. I like to be able to look at the numbers (and the rates of change) and be able to figure out if any of my revenue-generating strategies is working well or not.

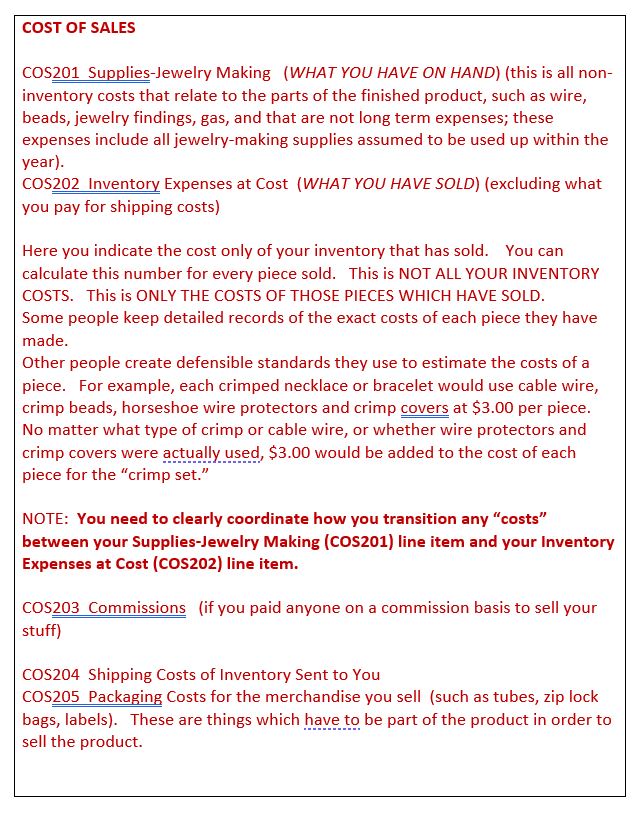

COST OF SALES

This is the most confusing part of the general ledger, because you have to make some rules and be clear about what you are calling “Supplies-Jewelry Making” and what you are calling “Inventory”.

As a Jewelry Making business, you wear many hats – you are the manufacturer, the distributor and the retailer. The tax laws are written in a way that assume you are one or the other – not all three at the same time.

At this point in the ledger, you can calculate the first of two Magic Numbers – Gross Profit. If using a spreadsheet, you can put the formula into one of the cells of the table.

| MAGIC NUMBER (Gross Profit): Your REVENUE minus COST OF SALES equals GROSS PROFIT. |

If your GROSS PROFIT divided by your REVENUE is greater than .50,

then you’re doing well.

With the Magic Numbers, you have some easy to access and interpret information to help you financially manage your business. You look at month-to-month and year-over-year trends. When you first get started, some of these Magic Numbers might be on the not-so-good-looking-side, but again, pay attention to trends.

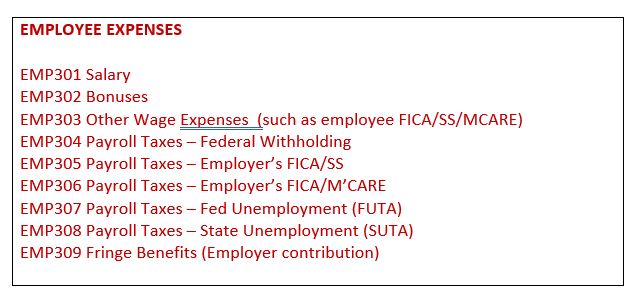

EMPLOYEE EXPENSES

(These are the minimum number of employee line items you will need to be able to fill out all the Federal, State and Local payroll tax related forms. You can always add more categories than those stated here.)

If you have employees, it may make sense to pay for a payroll service, that both cuts the checks and does your quarterly and annual payroll taxes.

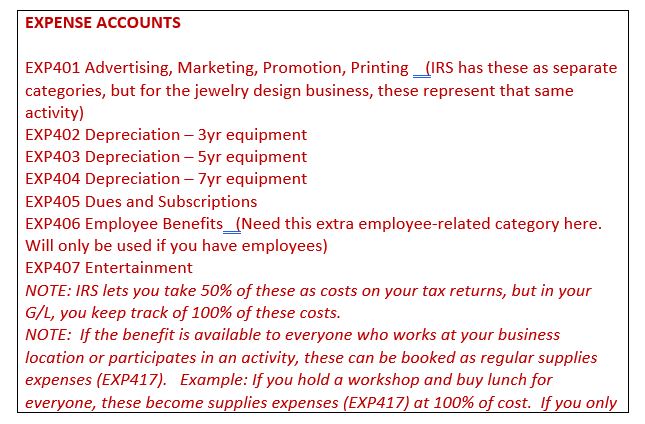

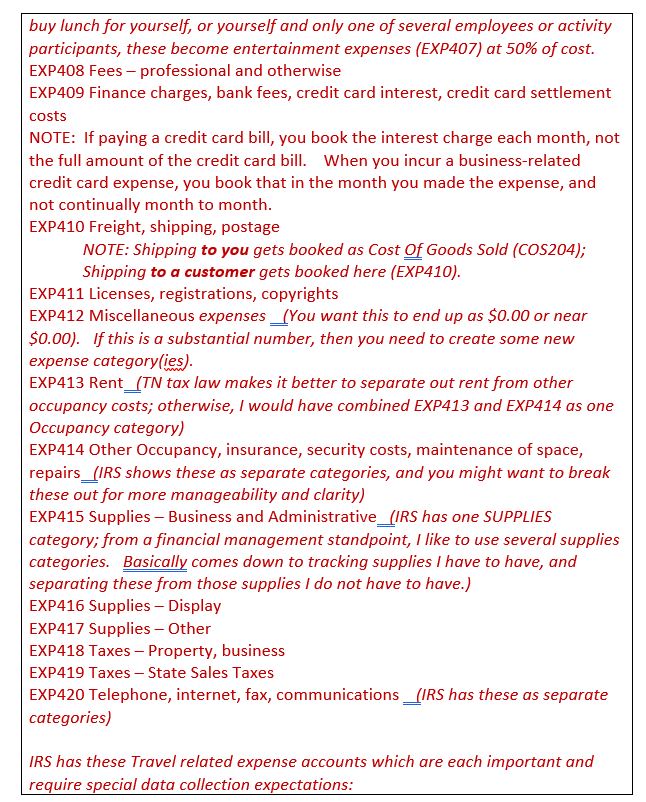

EXPENSE ACCOUNTS

Your expense accounts are how you track what happens when you spend money.

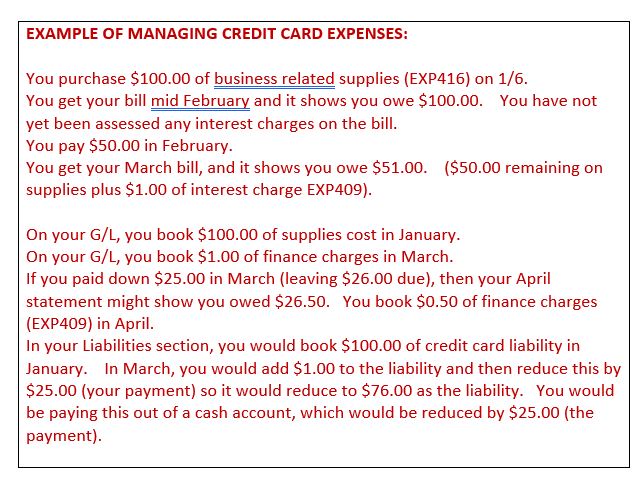

Sometimes it gets a little confusing how to enter credit card expenses into your general ledger.

Now you are positioned to calculate the next Magic Number – Net Profit.

| MAGIC NUMBER (Net Profit): Your REVENUE minus COST OF SALES minus EMPLOYEE EXPENSES minus all other EXPENSES equals your NET PROFIT. |

You want this to be a positive number. However, for your first year or two, it might be negative. Again, it’s most useful to look at trends.

NOTE: There is NO IRS rule that says you have to show a profit in 3 of the last 5 years, or any rule about the frequency of profit. As long as you a trying to run a business as best you can, even if you are failing miserably, there are no consequences for showing continued losses.

In a double-entry system, the other part of the general ledger will account for

a) ASSETS

b) LIABILITIES

Example: You buy $10.00 of beads.

| Debit Inventory by +10.00 | Credit Cash by -10.00 |

| (increases inventory total by 10.00) | (decreases your cash by 10.00) |

Assets are things you own and have value for your business.

| ASSETS 501 INVENTORY (See discussions of inventory above) 502 PREPAID EXPENSES 503 PEOPLE WHO OWE YOU MONEY 504 NON-COMPUTER EQUIPMENT 505 COMPUTER EQUIPMENT 506 FURNITURE 507 ACCUMULATED DEPRECIATION |

Liabilities are things you owe to others, which until these are paid off, decrease the value of your business.

| LIABILITIES 601 PAYROLLTAXES 602 OTHER TAXES 603 SALES TAXES COLLECTED 604 GIFT CERTIFICATES OUTSTANDING 605 NOTES PAYABLE – BANK 606 CREDIT CARD #1 607 CREDIT CARD #2 |

You now have in place a system for gathering information about money costs and money revenues. You need to expand this system to gather even more detail, specifically about your inventory.

c) ROI: Inventory Management

The Kinds Of Things You Want To Be Doing

In Inventory Management

Monitoring and managing inventory involve several interrelated activities. These activities will place time and cost burdens on you. Luckily, much of this can be computerized. There is inventory management software available, some of it specialized for jewelry. If you are selling things online, your shopping cart system will accommodate a lot of this.

These activities include:

- Par Levels

- Storing and Tracking FIRST IN, FIRST OUT

- Supplier Relationships

- Resiliency

- Auditing

- Prioritizing

- Forecasting

- Timing

To the extent that you can systemize all this, relying on a central, computerized database, the more efficient and effective you will be. Ask yourself, as well, whether your inventory management system will grow with you as you continue to develop and expand your business. You always want to have the right stuff, in the right place, at the right time, at the right cost.

- Inventory Management: Establish Par Levels

What is the minimum inventory needed on hand at all times? For example, when doing craft and art shows, you will need to have 4x the amount of inventory from what you want to sell (thus, $1000.00 of inventory to sell $250.00 of merchandise).

Do you have a tickle system signaling times to reorder?

What have you based your par levels on? Sales rate? Time it takes to acquire items?

If demand changes, do you have strategies for adjusting your par levels?

Do you need to maintain any samples of your work which never get sold, but are used for displays, promotions, or photography?

Do you need to have finished pieces on hand, or will you make pieces to order on demand?

- Inventory Management: Storing and Tracking your FIRST IN, FIRST OUT (FIFO)

You want your oldest stock to get sold first.

Are your things stored and displayed to meet this principle?

Do you have adequate storage space? Containers?

What is it costing to you maintain your desired storage levels?

When stock doesn’t sell within a reasonable time, what are your plans? Deconstruct finished pieces and re-use the parts? Discount or write-off dead parts inventory?

- Inventory Management: Maintain strong relationships and communication with your suppliers

What is it about some suppliers that you like, or that you dislike?

Will they accept returns?

Can they handle special orders?

If something is not currently available, can they tell you when it will be in stock again?

Will they work with you to waive minimums?

Do you have back-up suppliers in case your primary supplier can’t come through?

- Inventory Management: Maintaining Resiliency and Doing Contingency Planning

You need to actively and continually do What If Analysis.

What if…

- An item becomes especially popular?

- You run out of cash?

- Storage becomes an issue?

- Your tracking and data system somehow goes awry?

- Parts become unavailable or are discontinued?

- Parts or merchandise are damaged or spoiled?

- Customer wants, needs, demands, desires or shopping behaviors change?

- Other unforeseen circumstances?

Do you have any part of your inventory set aside for use in case of an emergency?

- Inventory Management: Auditing your inventory on a regular basis.

Auditing will include a mix of big, scheduled activities and some spot checking. Auditing means establishing a baseline. It means identifying current inventory challenges. It means evaluating your current procedures and data systems, and identifying their strengths and weaknesses.

- Inventory Management: Prioritizing Inventory by Value.

Some value might have to do with how much something contributes to revenue and profitability. Items with higher mark-ups would get more attention.

Some value might have to do with the rate of turnover. Items more popular and sell faster would get more attention.

For management purposes, it might be useful to establish 3 groups of value. Group A might represent things contributing 50% of value. Group B might represent things contributing 35% of value. Group C might represent things contributing 15% of value.

- Inventory Management: Forecasting.

You want to be in a position where you can predict future demand, perhaps over the next year or two. You want to be able to define seasonality fluctuations. You want to anticipate the impacts of any upcoming promotions or advertising. Much of forecasting involves tracking your orders/sales and relating this back to inventory.

- Inventory Management: Timing.

What time issues/management would be associated with maintaining the lowest inventory possible to meet your demand. Here you tried to understand if you can shift the costs of storage and securing supplies over to your suppliers. Customers these days often demand immediate satisfaction, so shifting some costs to supplies may be problematic for you.

The systems you have built to track, maintain and analyze your money flows and your inventory are sustained by a whole set of receipts and administrivia related to banking, insurance, credit card processing, travel, and working with employees and independent contractors.

d) ROI: Other Record Keeping

You want to keep all your receipts together for each calendar year. You do NOT want to keep all your receipts stored in a shoe box. File your receipts, say in an accordion file, organized alphabetically by company.

If part of the transactions listed on any receipt are personal and some are business, then circle the business related ones and write something like “business” next to these.

If you did not get a receipt for something business related, write out your own receipt, with the date, purpose, description, and amount.

You must store these receipts (and your other business documentation) for 10 years. Some places list 7 years, but you will need to store these for 10 years.

Don’t rely on paying an accountant to sort through all your receipts in order to calculate your tax liabilities each year. The cost of this would be prohibitive. You yourself need to do that kind of leg-work, and being very organized will help you do this efficiently and effectively.

You probably will also be generating these kinds of forms and documents in the course of doing business, and you need to maintain files of back up copies:

- Purchase orders

- Invoices

- Packing slips

- Order sheets / line forms

- Catalogs

- Checkbooks, and copies of checks written or check requisition forms with check numbers of checks written documented

- State, local and federal tax documents

- Leases / rental agreements for property and equipment

- Account numbers and agreements with each of your suppliers and creditors

- Travel logs

- General Ledger entry forms

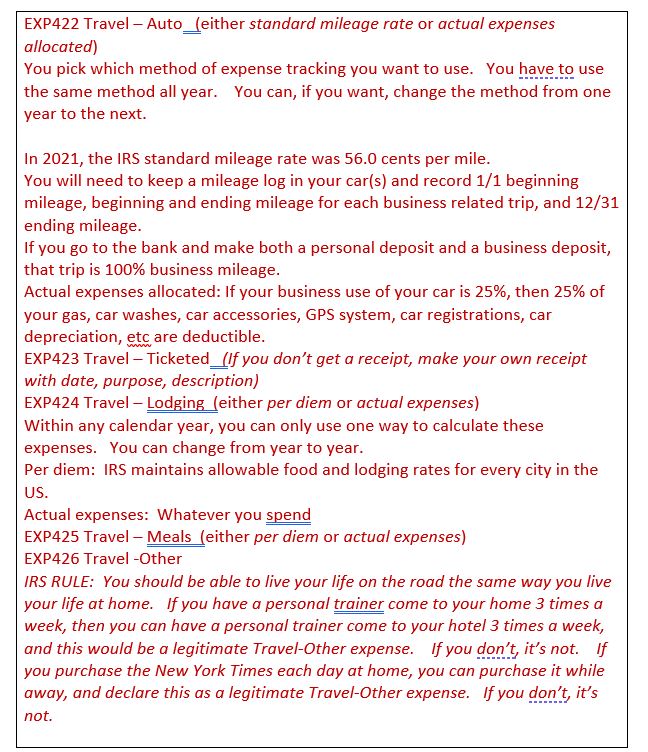

TRAVEL LOG

All your business travel is deductible, but the IRS has different rules for how you handle various business expenses. So, you keep separate accounts of

– Auto expenses (gas, depreciation, mileage, car maintenance and repairs);

NOTE: On your income taxes, you can use either a standard mileage rate or actual expenses allocated. You pick which method of expense tracking you want to use. You have to use the same method all year. You can, if you want, change the method from one year to the next.

– Meals while traveling;

– Lodging while traveling;

NOTE: Within any calendar year, you can only use one way to calculate these expenses. You can change from year to year. Either use Per diem (IRS maintains allowable food and lodging rates for every city in the US) or Actual expenses (whatever you spend).

– Ticketed travel (plane, boat, railroad, taxi, limo, ferry);

– Other travel expenses (newspaper, shoe-shine, gym).

NOTE: IRS RULE: You should be able to live your life on the road the same way you live your life at home. If you have a personal trainer come to your home 3 times a week, then you can have a personal trainer come to your hotel 3 times a week, and this would be a legitimate Travel-Other expense. If you don’t, it’s not. If you purchase the New York Times each day at home, you can purchase it while away, and declare this as a legitimate Travel-Other expense. If you don’t, it’s not.

Keep a travel log in all your cars, and record:

DATE, BEGIN MILEAGE, END MILEAGE, subtract to get TOTAL MILEAGE.

Write down the business purpose of each trip.

For example, if you’re in business selling beaded jewelry, you can deduct all your mileage for all your trips to any bead or craft store, any bead society meeting, any bead-related or jewelry-making classes, any trip to a museum to see jewelry on display, any trip to a store to do research on jewelry, check out the competition, mail bills at the post office, go to the bank to make a deposit, and the like.

BUSINESS CARDS

A must!

LOGO

This can simply be how you print the name of your business – font choice, layout, positioning of words. Or it can be a fancy image.

There are Logo-Maker apps online that you can try.

Once you get your logo, you will want to place it on all your forms, documents, marketing materials, and online webpages.

You will want to trademark your logo.

e) ROI: Employees and Independent Contractors

Sometimes you need to work with help. You might hire part-time or full-time employees outright. You might pay someone on commission or per piece where that person works as an independent contractor rather than an employee. You might barter and trade teaching someone some skills in exchange for some work, like hiring an unpaid intern or apprentice.

In these situations, you will need to anticipate if, after paying someone, and with employees also paying additional taxes, you can still make a profit.

Some forms to pay attention to:

With hired employees:

forms W-4 (when hired)

forms W-2 and W-3 (annually)

With independent contractors:

forms W-9 (before contract gets implemented)

forms 1099-MISC and 1096 (annually)

f) ROI: Banking, Insurance and Credit Card Processing

BANKING

BANK ACCOUNT: It is better to have a separate bank account for your business than for personal. If you use a personal bank account for your business, it is a good idea to have your bank-checks printed up in the business-check size. If you are a solo proprietorship, you would print your name on the checks, and under your name, you would print your doing business name as (DBA), as in:

Janet Jackson

DBA Retro Jewelry Designs.

If you have employees, it is useful, from a financial management standpoint, to have a separate business bank account that is dedicated to all payroll expenses (salaries and taxes).

Whether you are using a personal or business banking account, be sure to print your checks using the Business Check format. On your business checks, it is a good idea to have checks with your business name on it. You can either open a Business Checking Account, or have your business name printed on your Personal Checking Account checks. If printed on your personal checks, then again, you list your own name (which is your official business name) on the check, and under your name, you list “DBA, Your Business Name”, where DBA stands for Doing Business As.

INSURANCE

At some point, you will need to purchase business insurance to cover liability and theft or loss of property (inventory and equipment) issues and medical issues (you or an employee getting hurt in the context of the job). In most places, running a business out of your home violates local zoning codes. You may not qualify for a company’s business insurance package if you are violating these laws.

REMEMBER: When working with any insurance agent, that agent is professionally obligated to report any violation of the law, including these zoning laws, to the authorities. This is true, even if your insurance agent is your sister!

So, when you discuss insurance with your insurance agent, you will need to pose your questions as “What If?” questions – “What If I were to start a business in my home” — rather than indicate you already have or absolutely intend to locate a business in your home.

USE OF A CREDIT CARD: It is a better idea to use a separate credit card for your business than for your personal uses. If you do use one card for both personal and business, be sure to mark all original charged invoices as to which use they refer to.

CREDIT CARD PROCESSING

Whatever location your business is in – home, storefront, craftshow – you will need to be able to take credit cards. Very few customers use cash nowadays.

You will need to be able to accept a lot of different credit cards: Visa, MasterCard, Discover, American Express. Ideally, you want to use a processing company that lets you accept all these cards.

You will need to be able to swipe a card, insert a card to have its chip read, as well as manually enter a card number without the card present. You might need to be able to let someone touch their phone to your credit card machine to do the transaction.

You may want to open a credit card processing merchant account. Or you might use a company that doesn’t require you having your own merchant account. In this case, you would be using that company’s shared account. Some prominent companies which do shared accounts include PayPal and Square and GoPayment and Stripe. With the internet, competition for credit card services has gotten so fierce, that many of the rates and combined costs have been converging. Using a company with shared accounts will reduce the various certification and reporting requirements associated with having you own account.

Check your options online and do some serious comparisons here. Comparisons will not be straightforward because different companies which offer credit card processing services make their money in different ways. They will be inexpensive on some things, and more expensive on others. Some companies make money by leasing equipment. Others by charging you a fee for each sale (per transaction fee). Others by charging you a rate per dollar volume of each sale (discount rate).

Sometimes you can get used/rebuilt equipment very cheaply on line. But how cards are processed can change frequently, sometimes necessitating the purchasing of new equipment.

If you are locked into a multi-year lease on equipment or on credit card processing through a particular company, you will be liable for the expense through the end of the contract, even if you close your business before then. No-contract options are very appealing. One-year contracts are OK. Three-year contracts start to get risky, but may be an appealing option, given their whole package.

It is a good idea to check whether the credit card processing company has credit card scanning attachments that connect to your phone or tablet or operate with Wi-Fi. This is especially important if you are doing sales off site, like at a craft show.

Data systems are in place. Procedures are in place. Basic business relationships are in place. Now you need to create mechanisms to secure all this, that is, to secure the in-flows and out-flows of money so that you are taking the risks you want to take and achieving the rewards you believe you should get in return. These mechanisms include formal and informal arrangements and contracts, such as getting terms, getting paid, and crowd funding your business.

g) ROI: Getting Terms

Whenever possible, I suggest trying to get net terms with your suppliers. Net terms is a form of trade credit. Instead of paying upfront for your supplies, your suppliers will give you some predetermined period of time to pay for these goods. You get your supplies right away without having to pay until an agreed-upon future date.

Usually, you would get Net 30 terms, meaning you would pay within 30 days. Sometimes, if you have not paid within the terms set, you might get assessed a penalty fee.

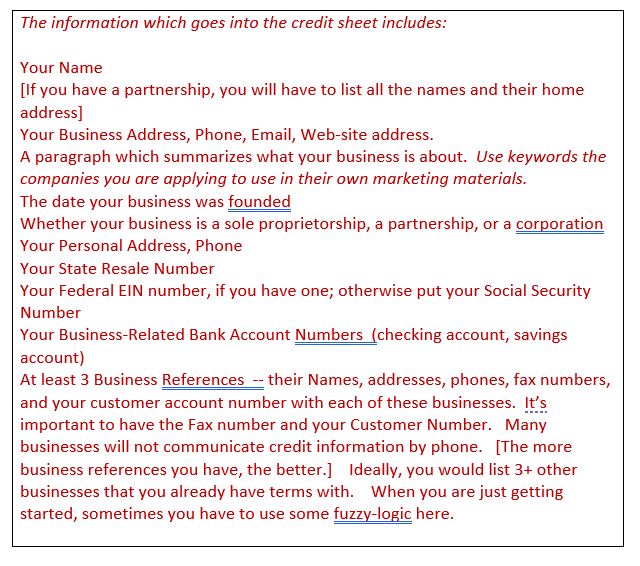

To apply for net terms with any supplier, you would submit a Credit Sheet.

CREDIT SHEET

You will want to prepare a Credit Sheet which lists the following information. You give this sheet to businesses where you want to apply for terms. When you buy things from businesses, you can pay cash (sometimes check or credit card) – this is considered Pre-Payment. You can pay COD (cash on delivery), but there is usually an extra COD charge tacked on. Or you can pay on terms or “on account”, usually signified as Net 30 or Net 10, where you would have 30 or 10 days to pay your bill. If you don’t pay within that time, the business may take away your privilege to buy on terms, or charge you a late fee.

h) ROI: Getting Paid

Getting paid for your work can range from the straight-forward to the nightmare. If you are doing a lot of custom work, your clients will probably pay you in increments, say 50% up front, and 50% upon completion. If you are doing a lot of consignment, the shops may pay for anything of yours that sells perhaps quarterly. If you are selling wholesale to other retailers, you might have extended them terms, say Net 30, where you expect to get paid at the end of the term period.

For each piece sold, or for several pieces sold at the same time, you will be generating some kind of invoice. Each month, you might also be following up with your customers with a statement form, showing what has been paid, and what still needs to be paid.

INVOICE or STATEMENT FORMS (2-part forms – one for you and one for your customer). You can get a blank pad at a local stationery store, or have these pre-printed with your business name, address and phone.

i) ROI: Crowd-Funding

Crowd-funding is when you seek funding from angel investors, government grants, loans or crowdfunding campaigns online, like with Kickstarter, to fund your creative pursuits. Crowd-funding creates financing opportunities. You might be looking to start a line of jewelry and mass produce and distribute it. You might be looking to franchise your business. You might have a product idea that you believe has great market potential. Jewelry products can be costume, semi-precious stones and metals (bridge jewelry), or fine jewelry.

Other crowd-funding platforms include Indiegogo and Ivylish. These provide a great opportunity for upcoming and small jewelry businesses who have an especially marketable idea. Each site has rules, requirements and fees. It is important to research what types of jewelry projects are most successful and least successful on each site.

The most popular crowd-funding campaigns offer a reward to the backers. This could be in the form of product, money, or an opportunity to participate in an event.

Crowd-funding gives the designer an opportunity to pre-test his or her ideas and how the market will respond to these ideas.

Some pointers:

- Pitches with video presentations work best

- Have clear and concise goals; any potential backer should be very clear about the parameters of your project and what their money should be going towards

- You want your audience to be able to visualize your project; show them in images what you have done before, and what you hope to do with this project; make them want it

- Reach out to your inner circle first, and evidence of their backing will legitimize and validate you and your project as you reach out to the larger market; enlist them as deputized marketers, asking them to spread the word, increasing your visibility and exposure, through their own social media connections

- Name your donation levels in a clever and tied-in way; you might point out that they could donate the price of a coffee or price of a cab fare to make it easier to understand how to donate to your campaign

- It helps to offer samples of your work or promotional items like stickers, posters, autographs, even T-shirts with your products branding on these

- The campaign will be a commitment of time and energy; you will always be hustling; no time to sit back and watch

- Keep your backers up-to-date with posts, newsletters, whatever

- If your donations slow down to a trickle, try a new approach to your marketing

- Remember, many campaigns reach their final goal in the eleventh hour

Accounting, bookkeeping, inventory management, record keeping, business relationships with financial institutions and suppliers are in place. You still won’t be able to achieve that sweet spot between risk and reward without the appropriate business growth mind-set. In the creative marketplace, where your success relies on both your artistic/design, as well as your business, acumen, this can be difficult for you. But it can be done. With that right mind-set.

j) ROI: What Does It Mean To Foster A Growth Mind-Set

Failure is uncomfortable. Disconcerting. Too often, we do everything we can to keep ourselves out of situations where we might fail. We focus on what could go wrong, instead of what could go right. We think we don’t have the abilities to do the task. We get paralyzed. We do nothing. Or we keep repeating ourselves, producing the same-ole, same-ole, whether there is a continued market for these items, or not. Or we begin to visualize any risk as insurmountable, way bigger than it really is.

But allowing any fear of failure to become some kind of insurmountable wall works against us. If we are trying to make a go of it by selling our jewelry, we can’t build these kinds of walls. Successful business people and successful businesses need to foster a culture which promotes a growth mindset. Simply, a growth mindset is a culture where you have permission and encouragement and confidence to take risks.

Risks are OK because they bring rewards. Rewards allow the business to maintain itself, sustain itself, grow and expand. Failures are OK, as well, as long as they become learning experiences. Doubt and self-doubt are OK only if they are used to trigger reflection and new ideas to overcome them. Not having the skills requisite for the moment is OK because we are all capable of continual learning. Temporary setbacks are OK because you have had them before and overcame them.

Carol Dweck wrote the seminal book on growth mindsets called Mindset: The New Psychology of Success (2006), with a series of related books to follow. People have either a growth-mindset or a fixed-mindset.

Those with a growth-mindset believe their abilities are developed through continual learning and hard work. They are more willing to experiment and try new things, and see failures as opportunities rather than set backs.

Those with a fixed-mindset believe that abilities are innate – you’re born with talents or not. They seek out opportunities where specific talents, rather than effort, leads to success. They prefer to repeat tasks and apply skills they are already familiar with.

Developing a growth mindset means such things as…

- Understanding the power of “Not Yet”.

- Setting learning and continual learning goals

- Being deliberate and constantly challenging yourself

- Asking for honest feedback and criticism

- Always reflecting on and being very metacognitive about your thoughts and actions, successes and failures

- Recognizing if you are stuck in a fixed-mindset, and acknowledging your weaknesses

- Focusing on the process, and less-so on the result

- Getting comfortable with self-affirmation, rather than needing the affirmation and approval of others

___________________________________

FOOTNOTES

Campbell, Casandra. What Is Inventory Management? How To Track Stock For Your Ecommerce Business, Inventory Management, 6/19/20.

As referenced in:

Inventory Management

Caramela, Sammi, 10 Essential Tips For Effective Inventory Management, Business News Daily, 4/15/2020.

As referenced in:

https://www.businessnewsdaily.com/10613-effective-inventory-management.html

Dweck, Carol. Mindset: The New Psychology of Success, 2006

Fundbox.com. Trade Credit: Everything you need to know about net terms for your business. n.d.

As referenced in:

https://fundbox.com/resources/guides/trade-credit/

Shah, Vyom. Crowdfunding the Jewelry business, 11/27/14.

As reference in:

https://betterdiamondinitiative.org/crowdfunding-the-jewelry-business/